🇨🇳 THE CHINESE STUDIO TAKING $28M A MONTH FROM WESTERN CASUAL GAMING

A merge puzzle about a cheating husband is generating an estimated $28 million a month from US players alone.

The studio behind it - Microfun, based in China is now the third highest-grossing Chinese mobile publisher in the world. Behind only Tencent and Century Games.

Most people in Western mobile gaming still haven’t heard of them.

Here’s the full story.

The sequence

2022: Microfun launches Gossip Harbor globally. The premise is simple: a woman discovers her husband is cheating, divorces him, returns to her family’s dilapidated restaurant with her daughter, and starts over. Players help her rebuild it through merge gameplay, combining ingredients, serving customers, uncovering the story.

The target demographic is US women aged 25-45. The aesthetic is vibrant, saturated, deliberately feminine. This was not an accident.

2024: Revenue grows tenfold in a single year. The US accounts for nearly 50% of all earnings. By November, Gossip Harbor surpasses Travel Town, the previous merge category leader, to become the highest-grossing merge game on Google Play globally.

2025: The game reaches an estimated 28 million monthly active users. Estimated lifetime revenue crosses $720 million.

2026: Microfun overtakes NetEase to become the #3 Chinese mobile publisher worldwide by overseas revenue. One title powered a studio past one of China’s largest gaming companies.

How they actually did it

The numbers are interesting. The mechanism is more interesting.

Gossip Harbor does something most Western casual studios still don’t: it treats live ops as onboarding, not retention.

Most casual games introduce live ops events in month two, after players have established a habit. The events are a tool to bring people back. Gossip Harbor puts events, competitive mechanics, and time-limited offers in front of players in their first sessions. By the time someone understands the core merge loop, they are already inside the monetisation rhythm.

According to Balancy, a live ops platform that deconstructed the game in a March 2026 webinar, top merge titles now run 100+ live ops events per month. Gossip Harbor is among the leaders in event density. The offers are sequenced by price point, a $2.99 introductory bundle appears early, not to generate revenue, but to identify which players will spend and what they respond to. It is behavioural sampling disguised as a promotion.

The result is a 4.63 App Store rating with 575,000 reviews. At that review count, that rating is not luck. It is a product that people genuinely enjoy, despite (or because of) its aggressive monetisation design.

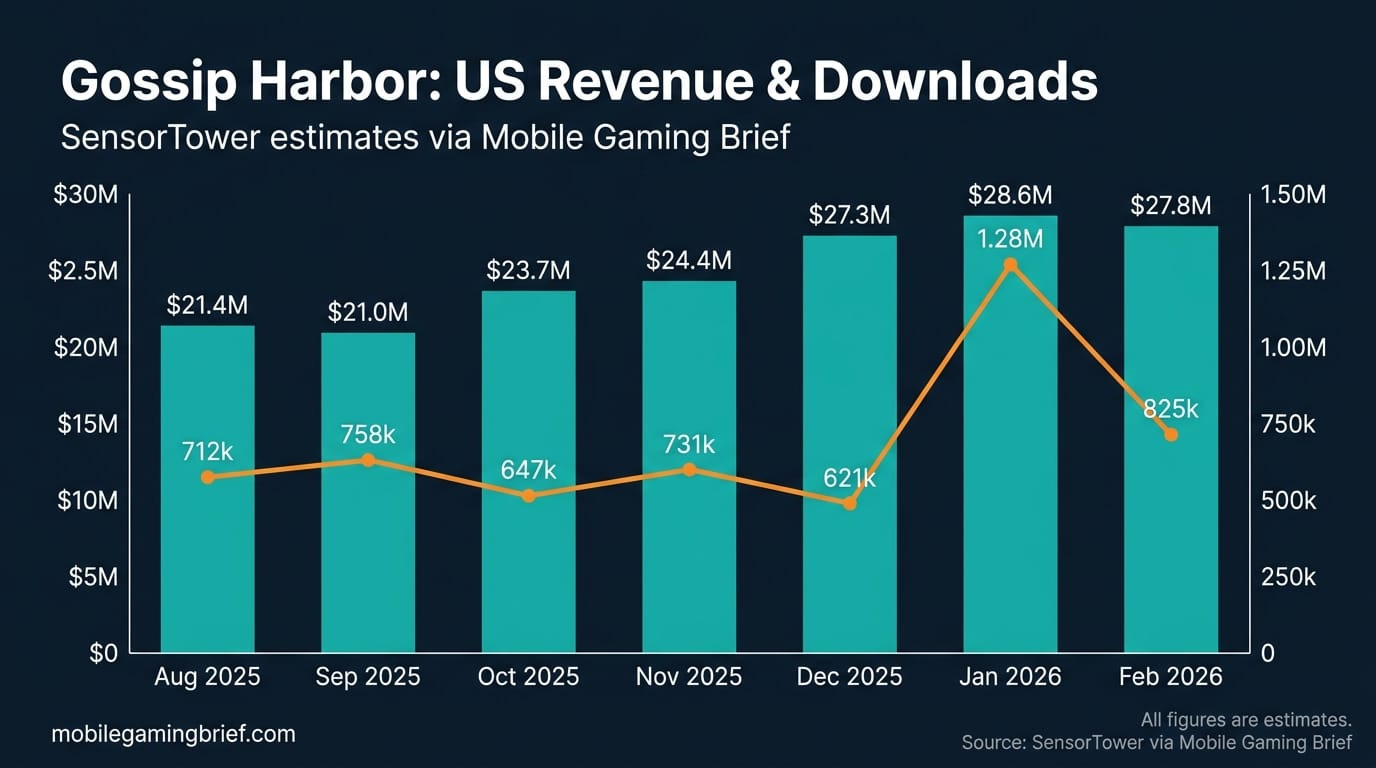

The data

Our analysis of SensorTower estimates shows Gossip Harbor’s US revenue trajectory over the past seven months:

All figures are SensorTower estimates. Revenue is in USD.

That January spike of 1.28 million downloads, $28.6M revenue, is not organic. Microfun ran a major UA push into the new year window, a period when casual CPIs drop post-holidays and competition for impressions falls. They timed it precisely.

The market shift behind the game

Gossip Harbor is not an outlier. It is evidence of a structural shift in who is winning the US casual market.

Our analysis of US top chart data across the past six months shows the Casual/Puzzle category has taken 0.9 percentage points of download share from Action games. Action is the biggest loser. Casual is the biggest gainer. And the studios leading the casual category right now are overwhelmingly operating with Chinese production discipline, even when they are not Chinese.

Dream Games (Turkey) is the clearest Western exception. Royal Kingdom pulled an estimated $14 million from the US in February 2026 alone, and Dream Games has the same design rigour as their Chinese counterparts: story-first, live ops from session one, UA spend concentrated on proven creatives.

But Dream Games is one studio. The broader pattern is:

• Microfun - Gossip Harbor, Seaside Escape, Flambé: Merge and Cook. A portfolio approach, same playbook across titles.

• Century Games - Whiteout Survival, Call of Dragons. Strategy and casual. $40M+ US revenue in February.

• FUNFLY - $51M US estimated revenue in February across two titles. Barely covered in Western press.

Three Chinese publishers generating a combined estimated $124M from US players in a single month.

What this means if you’re buying casual inventory

Casual is getting more expensive on the buy side. Chinese publishers are pouring UA budget into Western markets. CPIs in casual are rising as a result.

The games winning organic chart position right now are not the ones spending least. They are the ones with the tightest live ops cadence, which drives the retention that makes paid UA profitable. Higher retention means higher LTV means they can outbid everyone else for the same inventory.

If you are buying rewarded or casual placements and your publisher partners are not running aggressive live ops, you are buying into declining LTV. The benchmark is shifting and it is shifting fast.

Sources

• Revenue and download data: SensorTower estimates via Mobile Gaming Brief analysis

• Gossip Harbor US market growth 2024: Mobidictum, January 2025

• Live ops design analysis: Pocketgamer.biz (http://pocketgamer.biz/) / Balancy webinar, March 2026

• Microfun publisher ranking: SensorTower estimates, March 2026

• App Store rating and review count: SensorTower app metadata, April 2026

All revenue figures are third-party estimates. Mobile Gaming Brief does not have access to internal studio financials.